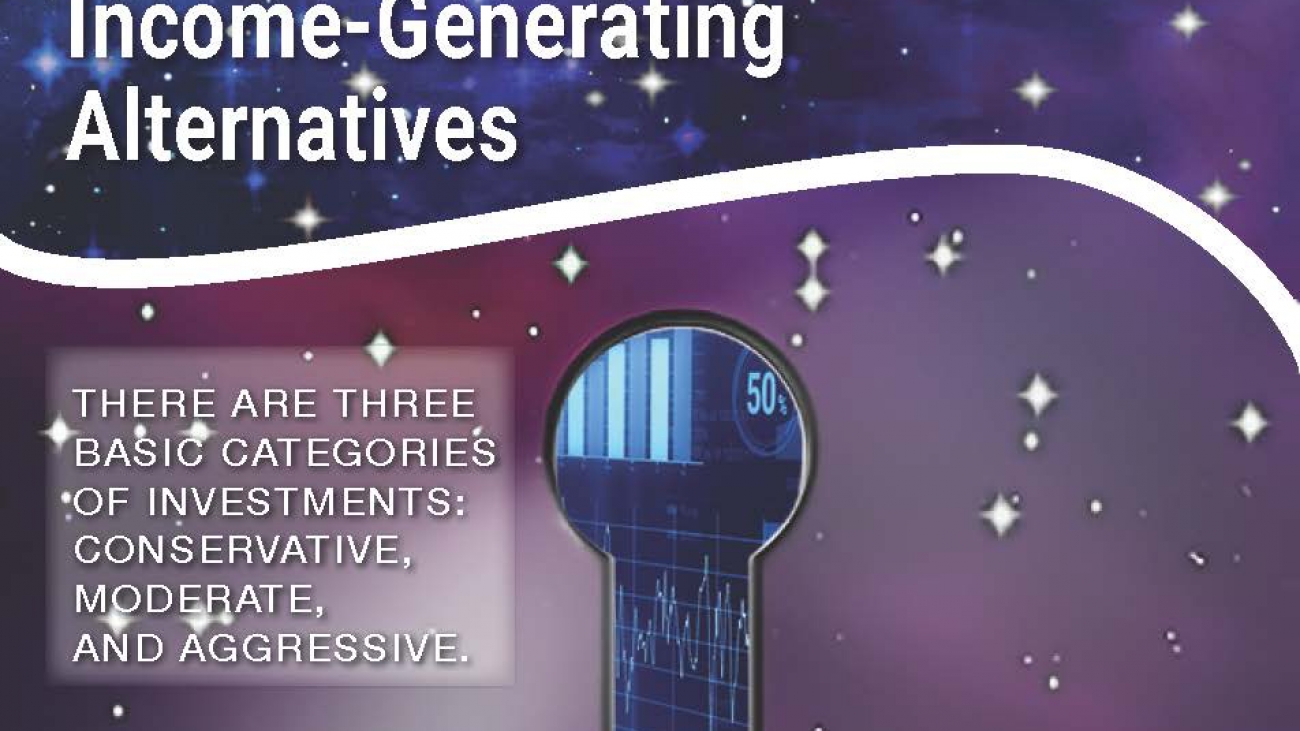

There are three basic categories of investments:

• moderate

• conservative

• aggressive

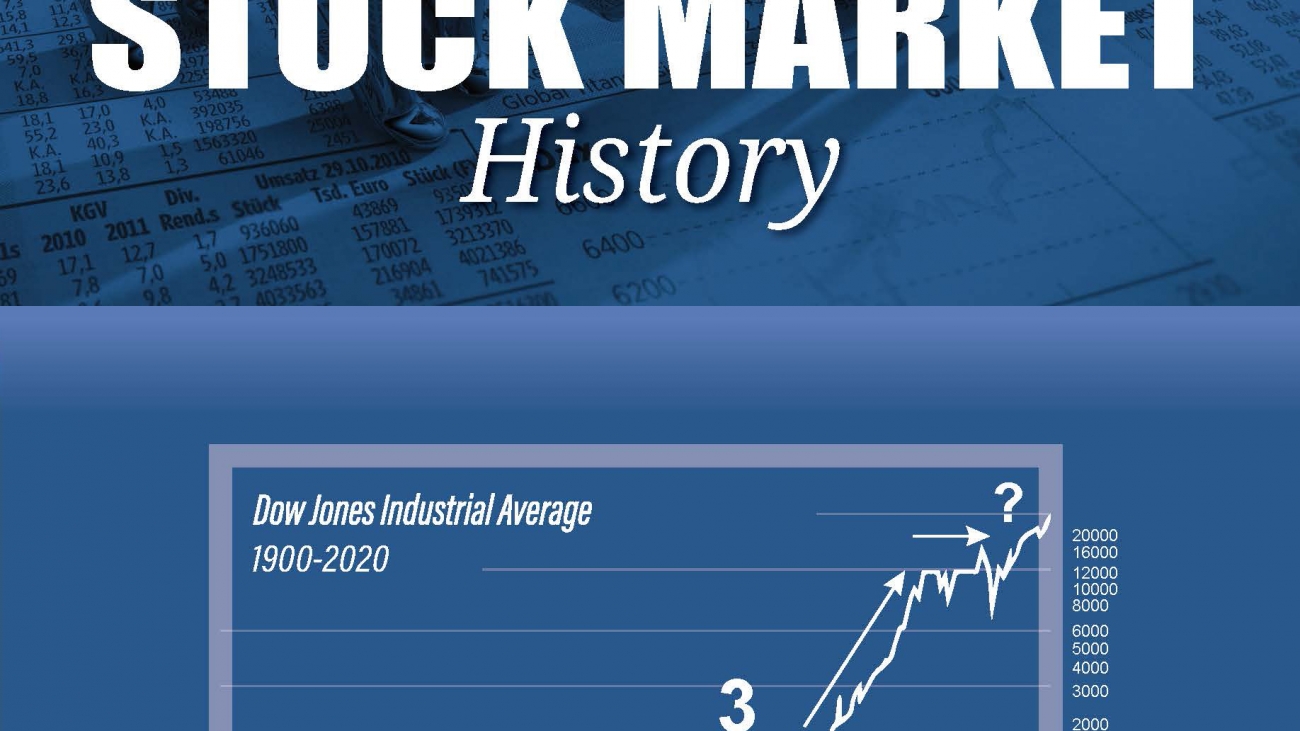

Aggressive instruments are those primarily invested in for growth. As the chart shows, they include things such as common stocks, stock mutual funds, commodities, and speculative real estate. Again, these are typically invested in for growth or capital appreciation, not income. They are considered aggressive because, while they can provide large short-term gains, they can also cost the investor large, sudden losses.